Dividing Financial Assets During a Chicago Divorce

Attorneys Handling Chicago Divorce Cases Involving Division of Stocks, Pensions, Bonds, and Trusts

Divorce is a difficult process. Giving up a shared life can also mean giving up what you have jointly earned or acquired as a couple. Hiring a competent Chicago divorce lawyer who understands the law can make property division in Illinois less stressful, so speak to Nottage and Ward, LLP, at (312) 332-2915.

Complex Assets

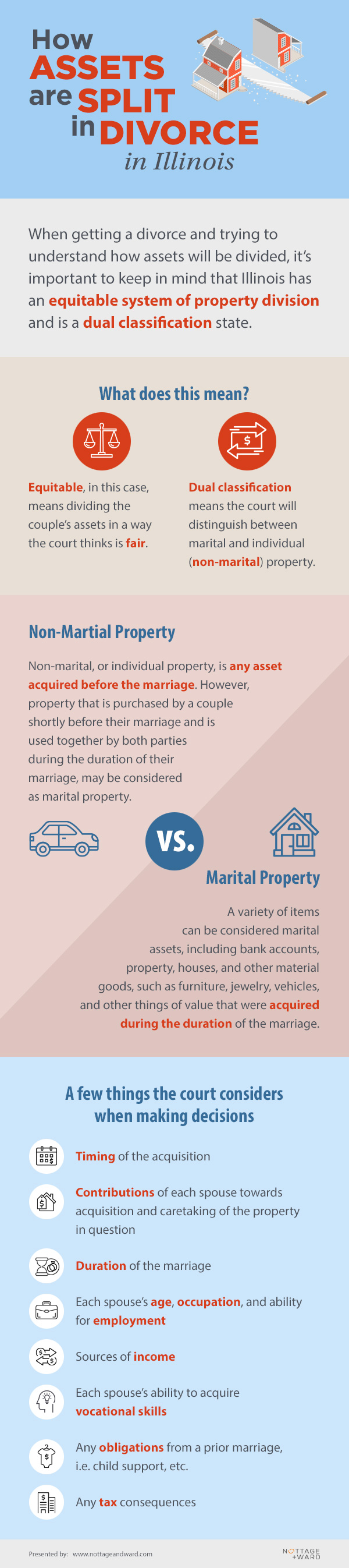

Some of the hardest assets to divide are pensions, retirement plans, insurance policies, and stock options. These may not only have property interests, but may also be treated as income, either of which may trigger tax and other federal obligations. In Illinois, state law calls for the equitable division of property, but other jurisdictions may require consideration.

Equitable, in Illinois law, does not mean an equal division of property, but looking at property-based factors such as marital or individual property, abilities of each spouse to earn a living after divorce, and health.

While some couples may be able to agree how to divide their property without a trial, some couples can’t agree or the properties are too complex for simple division. In these cases, a judge in the Illinois Circuit Court will divide the marital estate following a trial prior to granting a Judgment of Divorce.

It is wise for each spouse to hire an attorney who provides forensic accounting. An attorney who provides forensic accounting will track down, catalog, and value the joint property to present as evidence to a judge. This is especially important for finding hidden assets, or dealing with complex issues of retirement benefits, pensions, stocks, or bonds.

"...the settlement was more than I could have hoped for. But I am even more in awe of the way you dug into the financial details..."

- Susan

Getting Retirement Benefits

Retirement benefits are assets that many spouses own jointly even if the retirement account is in only one spouse's name. They are often marital property because of contributions made from income earned during the marriage or comingling of funds, which may require an analysis of the appreciation of assets during the marriage.

To obtain qualified retirement assets, a divorcing spouse must have a Qualified Domestic Relations Order (QDRO). A QDRO, according to the IRS, is a judgment for a retirement plan to pay marital property rights to a spouse or former spouse. The QDRO judgment should have specific information, such as the retirement participant's and alternate payee's name and address as well as the amount of the participant's benefit to be paid to the other spouse (the alternate payee). The alternate payee receives and reports the QDRO benefits as if the payee is a plan participant. The receiving spouse may be able to roll over, tax-free, all or part of the distribution from a qualified retirement plan. Pensions, like retirement benefits, require a QDRO. The exceptions are Social Security benefits and Tier I Railroad Retirement benefits, as well as some IRAs which do not require a court order.

Deferred compensation plans, like IRAs, 401(k)s, and other programs, can be liquidated before the normal age of retirement. As such, they can be divisible as a form of cash asset during divorce proceedings, but may trigger significant tax consequences.

Insurance Policies

Common types of insurance, such as automobile, homeowner, and property policies typically follow the asset that they are insuring and become the obligation of the party who is keeping that asset.

Under federal law, medical insurance companies are required to provide health insurance coverage for up to 36 months following a divorce to the employee’s former spouse, after which time that spouse must apply for independent coverage.

Life insurance, disability, and other policies that involve specific cash values are particularly important when going through a divorce. Divorcing couples have the option to liquidate their policies and receive the cash value that has been accrued up to that point. However, this normally leads to their coverage being terminated. If couples wish to retain their individual coverage, there will need to be further considerations when settling the divorce. Such considerations include the circumstances in which the coverage was first obtained, whether one spouse relies on the other spouse’s livelihood following the divorce, and whether any future accident would impact the ability of one spouse to meet his or her agreed-upon financial obligations.

Tax Credits

When couples have shared tax credit claims like children, it can make the already complicated process of divorce all the more overwhelming. The simplest answer to the question of which spouse can claim a child as a tax credit is, the spouse who has primary allocation. The other parent or guardian may be able to claim the child on their taxes only if the allocated parent freely gives up his or her right. The right to claim a child or children as a tax deduction is often negotiated by the parties before the divorce is finalized.

Of course, many divorcing couples end up sharing parenting time of their child or children, and this can complicate things further. Essentially, the IRS considers primary custody to rest on the parent with whom the children spend most of their time—even if it ends up being only a few more days out of the year. While uncommon, some joint parental allocation arrangements do involve an even 50/50 split in each parent’s time. When this is the case, the IRS will provide the deduction to whichever parent earns the highest adjusted gross income.

Stock Options

Other assets that a judge will divide are stock options. There are different considerations for stock options depending on when the options were given to the individual spouse. Options that were rewarded prior to a marriage may be individual property and belong to the initial owner. Stock options acquired after marriage are often viewed as joint property. One of the considerations to explore is how much of the vesting period took place during the parties’ marriage and what, if any credit should be given as a result. Options that serve as incentives for future loyalty and performance may or may not be joint property. This future nature of the "enticement" portion of the stocks may outlast the marriage and belongs to the individual spouse after divorce because the value of the stocks was not realized during the marriage.

Talk to a Chicago Divorce Lawyer

A competent Chicago divorce attorney can help to guide you through a financially complex divorce and handle issues you didn’t even realize could come up. For a comprehensive consultation on your situation, call Nottage and Ward, LLP, at (312) 332-2915.

Additional Information

- Accounting for Stakeholders in a High-Asset Divorce in Illinois

- Cryptocurrency in Divorce: What Happens to Your Digital Wallet?

- Handling Stock Options and Executive Compensation in Divorce

- The Future of Health Savings Accounts in an Illinois Divorce

We are proud sponsors of Little Black Pearl Art and Design Center.

We are proud sponsors of Little Black Pearl Art and Design Center.

To learn more, click here.

Proud Member of Friends of the Chicago River.

Proud Member of Friends of the Chicago River.

To learn more, click here.

Client Reviews

![]() 5 Leslie has been the strongest representation I could ask for

5 Leslie has been the strongest representation I could ask for

Leslie has been the strongest representation I could ask for in a very complicated, emotional matter. She has continuously looked out for my best interest and the best interest of my son. She is always prompt in getting back to me and in keeping me well informed about my case.

Read More Client Reviews![]()